There was a noticeable dearth in venture capital (VC) for startups over the past several months unless they happen to be in fintech and AI-related fields. The Middle East and the GCC region are experiencing a similar trend that focuses on AI and financial technology.

Venture funding focus

It looks like the outlook for creator economy startups is bleak at the moment. Global venture funding over the last quarter dropped 51 percent compared to the previous year.

Artificial intelligence (AI), meanwhile, continues to attract sizable funds with VCs flocking to startups building GenAI products and services. Some even command $1bn plus unicorn-style valuations.

Over 60 percent of this year’s Y Combinator demo startups seemed keen on developing AI apps, 300 percent more than in recent years.

The Middle East and Fintech

The GCC has witnessed a boom in funding for fintech startups, increasing by more than 400 percent from $200 million in 2020 to $885 million in 2022.

Venture funding in fintech in the Middle East and North Africa region rose to $925 million in 2022 from $587 million in 2021, an increase of 58 percent. The sector’s share of venture funding increased from 21 percent in 2021 to 29 percent in 2022.

A 2019 Milken Institute report predicted that by 2022, 465 fintech companies in the Middle East would raise over $2 billion in venture capital funding, compared with only 30 start-ups that raised nearly $80 million in 2017.

The Gulf is a breeding ground for the payment and money transfer industries. A recent survey showed that two-thirds of UAE residents increased the amount of money they sent home, and 51 percent said their families would land on hard times without the remittances they received.

The MENA region is steadily building its fintech sector. MENA region startups received more than $2.5 billion in funding in 2021 alone.

This region enjoys a young, educated, and growing population with some of the world’s highest mobile, internet, and smartphone penetration rates. It presents fertile grounds for financial innovation.

According to the IMF, the UAE saw noncash payments rising from 39 percent in 2018 to 73 percent in 2023.

Still, only 17 percent of consumers in the Middle East use digital banking compared with almost 60 percent in the U.S.

The IMF said fintech revenues are expected to increase from $1.5 billion in 2022 to $3.5–$4.5 billion by 2025 in the MENA and Pakistan.

Fintech in the UAE is developed primarily around ADGM and DIFC free zones. Bahrain and Saudi have adopted a consolidated approach using their central banks.

Read: Saudi fintech companies already double all of last year’s numbers

Digital Sukuk

Fintech companies and digital sukuk appear to have strong growth potential for the global Islamic finance industry in the MENA region in the coming years, according to Standard & Poor’s rating agency.

Traditional Sharia-compliant bonds, called sukuk, were developed as an alternative to conventional bonds. The global sukuk market was worth $193.2 billion in 2022, according to Refinitiv data, with the main issuers being Malaysia, Indonesia, and Saudi.

S&P has witnessed an increase in sukuk issuances driven by Saudi’s implementation of Vision 2030, an agenda aimed at diversifying the kingdom’s economy away from oil. It also saw growth in green and sustainability-linked sukuk.

The emergence of AI

AI has the potential to disrupt complex industries and level the playing field for all digital start-ups, especially those in fintech.

Fintech could use AI to solve analysis of complex data sets with near-perfect accuracy, and thus avoid inherent risks associated with bad calculations.

AI’s large language models (LLMs) have significantly reduced the cost of incorporating the technology for startups looking to scale up their smart apps and services.

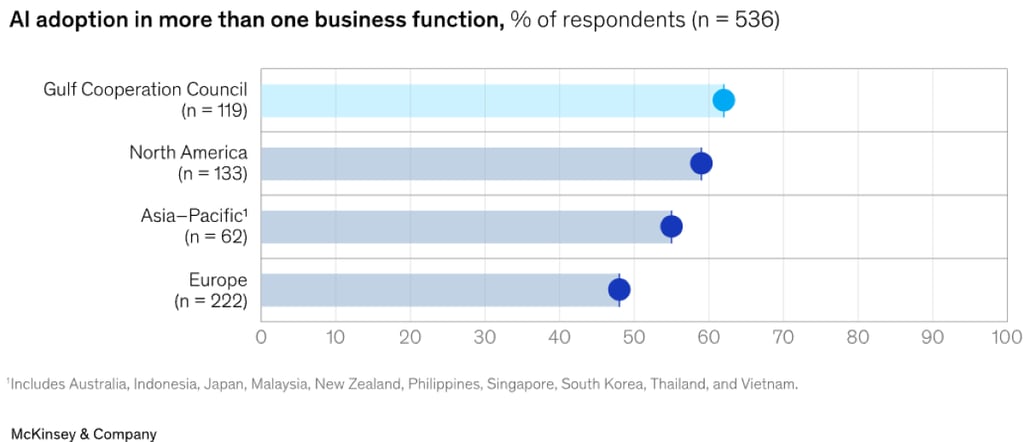

AI has the potential to deliver real value in the GCC, up to $150 billion, according to McKinsey research, or over 9 percent of Gulf countries’ combined GDP.

UAE’s DEWA has used an AI-powered virtual assistant to address around 6.8 million queries since its launch in 2017. Saudi Aramco’s Fourth Industrial Revolution Center claims it has reduced flare emissions by 50 percent since 2010 by using data and AI to monitor conditions and take preventative action.

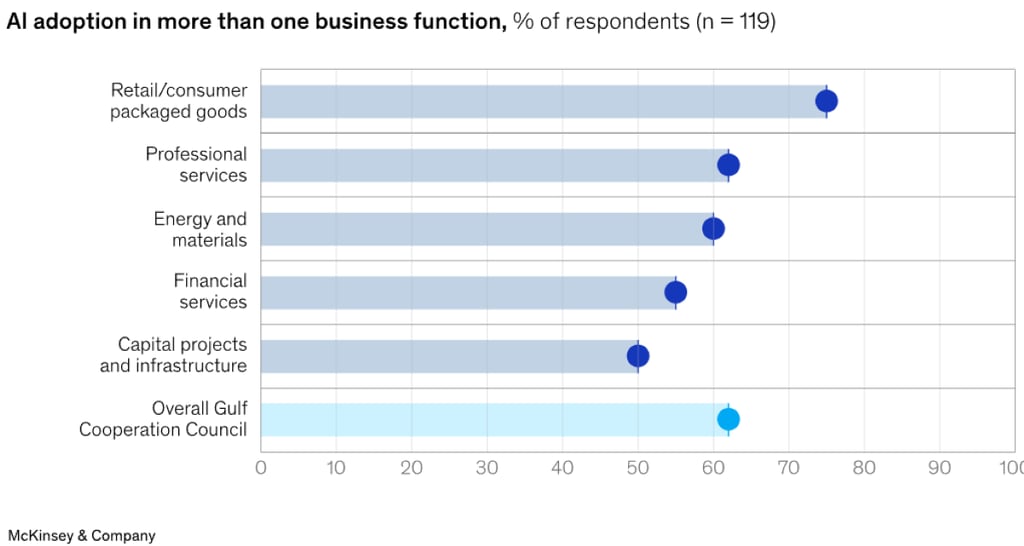

According to McKinsey’s survey, 75 percent of respondents from the retail sector say their companies have adopted AI in at least one business function.

Proper regulations, skills, and training are the top challenges facing the industry.

For more tech stories, click here.