The power transformer market in the Middle East is expected to grow with a CAGR of 10 percent from 2023 to 2030 in terms of revenue. According to the assessment of PTR, the growth will be largely driven by infrastructure development projects, expansion of transmission and distribution capacity, shift towards clean energy, and strategic initiatives within the region.

However, project delays, specifically in Saudi Arabia and Egypt, have the potential to slow down the growth in the power transformer market of the region. Interestingly, the regional power transformer market is moving towards localization, necessary to avoid high costs and supply chain issues linked with power transformers.

Market drivers

Several key factors are fueling the growth of the Middle Eastern power transformer market. These include significant infrastructure development projects, the expansion of transmission and distribution networks, the shift towards renewable energy, and strategic initiatives within the GCC.

Infrastructure development initiatives

Oil-rich Gulf nations are strategically shifting investments from oil and gas towards economic diversification, sparking a surge of major infrastructure projects across the Middle East. This increase in infrastructure activity is expected to significantly boost the demand for power transformers, as it requires improvements in grid connectivity and the integration of renewable energy sources.

Growth of electrical networks

By 2030, the Middle East is anticipated to add over 600,000 MVAs in transmission capacity, which will drive the demand for power transformers in the region. Specifically, Saudi Arabia plans to enhance the capacity of its high-voltage transmission substations by nearly 200,000 MVAs, leading to the construction of about 560 new substations and the installation of new power transformers by the Saudi Electricity Company (SEC).

Shift to renewable energy

The Middle East and Africa (MEA) region is expected to see a substantial increase in utility-scale solar capacity, with approximately 25 gigawatts (GWs) of new solar power anticipated. Saudi Arabia is particularly ambitious, aiming for renewable energy sources to comprise 50 percent of its energy mix by 2030 and setting a long-term goal of achieving net-zero emissions by 2060. Meanwhile, Dubai and Kuwait aim for renewable energy shares of 25 percent and 15 percent, respectively, by 2030. These ambitious targets are likely to drive a significant increase in demand for power transformers throughout the region.

Strategic plans in the GCC

Dubai’s Vision 2040 presents a detailed urban development strategy that could greatly influence future transformer demand. At the same time, Saudi Arabia’s Vision 2030 emphasizes economic diversification through various initiatives, which could reshape transformer needs as the country gradually moves away from an oil-dependent economy.

Project delays

The Middle East is experiencing significant shifts in its ambitious infrastructure initiatives, particularly highlighted by recent delays in Saudi Arabia’s NEOM project. A key factor contributing to this slowdown is touted to be financial uncertainty, which is apparently causing implementation delays.

Moreover, Saudi Arabia’s budget deficit is expected to continue at least until 2026, largely due to lower-than-anticipated oil revenues. To achieve a balanced budget, oil prices would need to remain around $86 per barrel, exceeding recent averages.

While Saudi Arabia navigates these hurdles, other Middle Eastern nations are experiencing varying outcomes in their infrastructure endeavors.

Hurdles for Egypt

Egypt, for instance, has heavily invested in infrastructure, including a new capital city of $58 billion. However, the country faces a severe economic downturn intensified by the pandemic and geopolitical tensions, resulting in currency devaluation and soaring inflation rates. The Egyptian pound has halved in value over the past 18 months, with inflation peaking at 36.5 percent in July 2023. Despite these challenges, foreign investments have emerged as a crucial support system, helping to sustain infrastructure projects and stabilize the economy.

Critical foreign investments in Egypt include a $35 billion agreement with the UAE for development rights along the Mediterranean and significant funding through China under the Belt and Road Initiative. Additionally, the IMF has agreed to provide a $8 billion financial package that will rely on economic reforms in the country.

These investments are vital for maintaining momentum in Egypt’s urban projects, with $3.9 billion earmarked for 2024-2025, highlighting the importance of foreign capital in overcoming domestic economic obstacles.

In contrast, the United Arab Emirates continues to advance its infrastructure projects without encountering similar delays. Abu Dhabi has approved 144 new projects with a total budget of nearly $18 billion, focusing on sectors such as housing, education, and tourism. The UAE’s proactive approach reflects a more stable economic environment, facilitating consistent infrastructure development.

Implications for the power transformer market

The delays and financial uncertainties impacting infrastructure projects across the Middle East have significant ramifications for the power transformers market.

Reduced demand

Slowdowns in major projects may lead to a decline in immediate demand for power transformers. Delays in these projects could postpone the installation of transformers necessary for electricity distribution and transmission.

Investment shifts

The reliance on foreign investments in Egypt indicates that the power transformers market may experience fluctuations depending on the stability and influx of these funds. If economic conditions deteriorate, funding for essential infrastructure upgrades could slow further, negatively affecting transformer demand.

Long-term demand

Countries like the UAE, which are actively advancing their infrastructure plans, may create growth opportunities in the power transformers market. As these projects move forward, there will likely be an increased need for reliable and efficient electricity transmission and distribution solutions in the long term.

Technological advancements

As the region aims to achieve its goals set for 2030, there is potential for growth in innovative and efficient transformer technologies, particularly those that facilitate the integration of renewable energy.

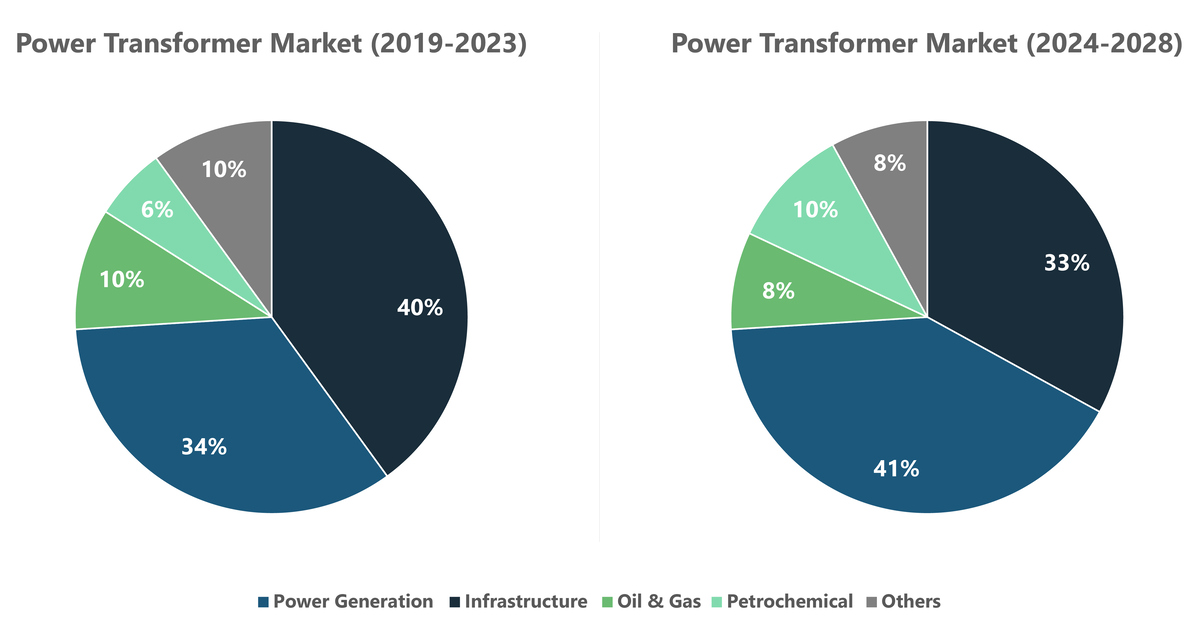

Future demand outlook

The future outlook for the power transformer market in the GCC region appears promising, with evolving sector dynamics influencing demand. From 2019 to 2023, the market was primarily driven by the power generation and infrastructure sectors, which together accounted for 74 percent of the share. Looking ahead to 2024-2028, while the infrastructure segment is expected to maintain its strong position, the power generation sector is projected to decline due to changing energy priorities and a slowdown in major projects.

The oil and gas sector is also anticipated to experience reduced demand, reflecting a decrease in large-scale developments. In contrast, the petrochemical industry will likely see significant growth, increasing transformer demand. Market spending is expected to rise, indicating a positive growth trajectory for the region’s power transformer industry.

Saudia Arabia

Saudi Arabia is advancing multiple large-scale infrastructure projects, such as NEOM, the Red Sea Project, and Qiddiya, all of which require substantial investments in electrical infrastructure, including transformers. Under Vision 2030, the country has set ambitious renewable energy targets.

As Saudi Arabia continues to move forward with tenders for major renewable energy projects, it is driving transformer demand. Additionally, the country is expanding its transmission and distribution networks to support increased renewable energy capacity and overall electricity demand while also investing in a green hydrogen-based ammonia plant as part of the NEOM initiative.

UAE

Dubai is committed to raising its renewable energy share to 25 percent by 2030 and 100 percent by 2050, prompting significant investments in its power grid and electrical infrastructure. The Dubai Electricity and Water Authority (DEWA) reported a notable rise in new transmission substations in the first half of 2022, demonstrating its commitment to enhancing the electrical network.

Furthermore, TRANSCO plans to significantly increase Abu Dhabi’s network capacity by 2026. Infrastructure projects like the expansion of the Etihad Rail network in Dubai are also expected to boost transformer demand due to the need for transformers for new tracks and stations.

Oman

Oman is set to emerge as the GCC’s third-largest transformer market, driven by Vision 2040’s emphasis on economic diversification and infrastructure development. The Oman Electricity Transmission Company (OETC) is investing in grid upgrades and plans to connect substantial renewable energy capacity by 2026.

Kuwait

Kuwait’s Vision 2035 aims to position the country as a regional hub, with major investments in infrastructure and power generation. The push for renewables, targeting 15 percent of electricity generation by 2030, will further drive transformer demand as the country upgrades its grid.

Qatar

Qatar’s transformer market is expected to see modest growth, primarily driven by Kahramaa’s expansion of the transmission network under the National Vision 2030. Major projects like the North Field East LNG expansion are also contributing to transformer demand.

Bahrain

Bahrain’s transformer market has experienced a decline following project completions, but the Ministry of Electricity and Water is working to expand the grid to achieve renewable energy goals, aiming for 10% of its energy mix from renewables by 2035.

Key OEMs

The market is primarily controlled by a handful of major companies, including Hitachi Energy, General Electric, Hyundai HI, Hyosung, Siemens Energy, and Elsewedy Electric, which together represent 60 percent of the market. An additional 35 percent is attributed by the ‘Others’ category, which encompasses companies such as Schneider Electric, SPTC, Iljin Electric, and Voltamp Transformers.

Despite not having local facilities in the region, Hitachi Energy, General Electric, Hyundai HI, Hyosung, and Siemens Energy together make up 52 percent of the MEA power transformer market.

Recent expansions

Oman-based Voltamp Energy Company has teamed up with Saudi Arabia’s Al Sharif Holding Group to establish a $10 million factory named ‘Saudi Voltamp’ to produce high-voltage power transformers. This joint venture aims to enhance regional manufacturing capacity, particularly in Saudi Arabia, which has historically depended on international suppliers due to limited local production.

The project aligns with Oman’s Vision 2040 for economic diversification and will be implemented in phases, with the first phase set to produce 132 kV transformers by 2025 and expanding to 380 kV by 2027, ultimately reaching an annual capacity of 30,000 MVA.

The need for local manufacturing is becoming increasingly important in light of rising import duties, supply chain challenges, and efforts to strengthen Saudi Arabia’s power grid while reducing dependency on imports.

In addition, Electrical Industries Company (EIC) has approved a $51.20 million expansion project for its subsidiary, Saudi Power Transformers Company (SPTC), located in Dammam. This project, set to begin in late 2024 and be completed by 2026, will enable the production of extra-high-voltage transformers and reactors, thereby increasing SPTC’s manufacturing capacity.

Currently focused on medium and large transformers, the expansion is designed to meet the growing domestic demand driven by major projects such as Neom City, King Abdullah Economic City, and the Red Sea Tourism Project. This initiative aims to reduce Saudi Arabia’s reliance on imported transformers, support infrastructure development, and facilitate the integration of renewable energy into the grid.

Looking ahead

According to the estimates of PTR, the power transformer market of the Middle East is set to grow with a robust CAGR of 10 percent in terms of revenue from 2023 to 2030. The majority of the growth will be driven by infrastructure development projects, expansion of electrical networks, shift to renewable energy, and strategic visions within the GCC.

The project delays, specifically in Saudi Arabia and Egypt, have the potential to dampen the growth in the regional power transformer market. However, localization efforts are a good omen as they are likely to reduce the high costs and supply chain issues mostly linked to power transformers in the Middle East. It is noteworthy that the majority of the demand for power transformers in the region is met through Western suppliers.

About the author

Syeda Maheen Mahmood is an analyst at PTR. She has focused her efforts on FACTs and HVDC topics before transitioning to the customs team. In her current role, she oversees various projects related to power converters, DC-DC contractors, data centers, transformers, and power quality equipment. Maheen delivers in-depth research projects to clients across North America and Europe, leveraging both primary and secondary research methodologies. With a degree in electrical engineering from NEDUET, she has been a vital part of PTR for more than a year, bringing a sharp analytical focus and a commitment to delivering actionable insights.

For more op-eds, click here.