Investment activity in MENA’s startup space slowed down in June 2024, as 38 tech startups raised $116 million, bringing the half-year total to $882 million, a new report suggests.

According to a Wamda research, the amount raised in June declined 59 percent month-on-month, but rose 182 percent when compared to the same period last year. UAE-based startups led the region in funding last month, securing $82.5 million across 15 deals. Egyptian startups followed with $15 million raised by four companies, marking the second-highest total. Saudi Arabia dropped to third, with seven startups raising $13.5 million. Notable activity was also observed in Iraq, with six startups raising an estimated $1.2 million, though this amount could be higher as Orisdi, BonLili, and Alsaree3 did not disclose their investment values.

Absence of mega deals in June

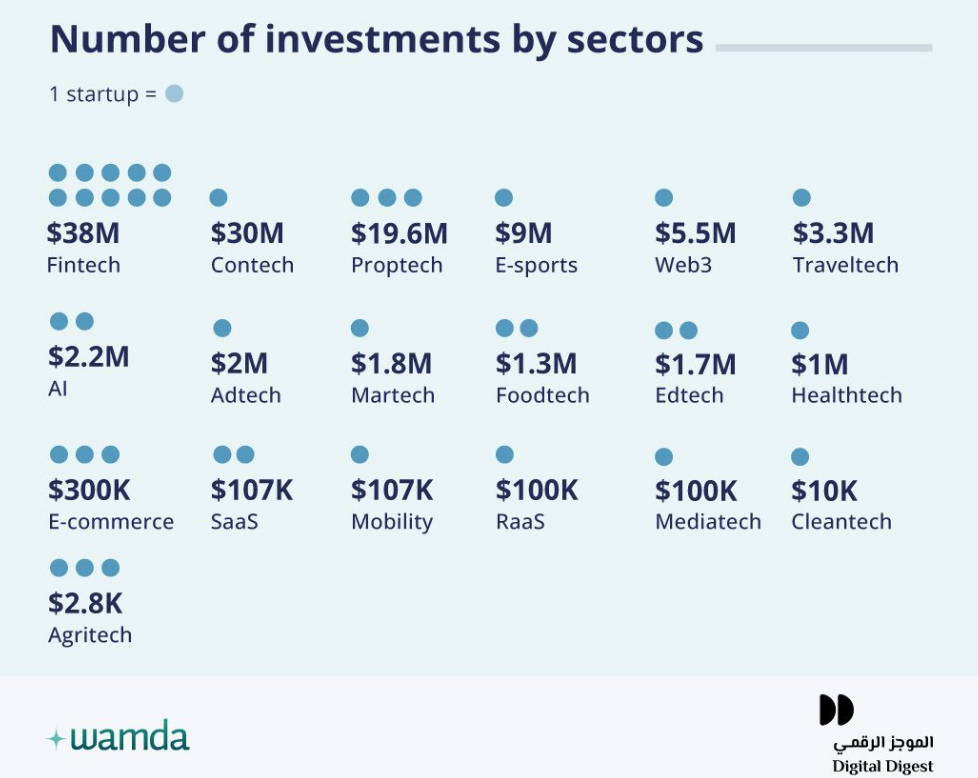

Last month was marked by an absence of mega deals, where the biggest ticket size in June went to Tenderd‘s $30 million deal. Sector wise, fintech reclaimed its position as the most funded sector in June, securing $38 million over 10 deals, closely followed by contech, thanks to Tenderd’s deal. Meanwhile, three proptech startups raised $19.6 million in June, reversing the lead it achieved in May.

Funding trends by stage and business model

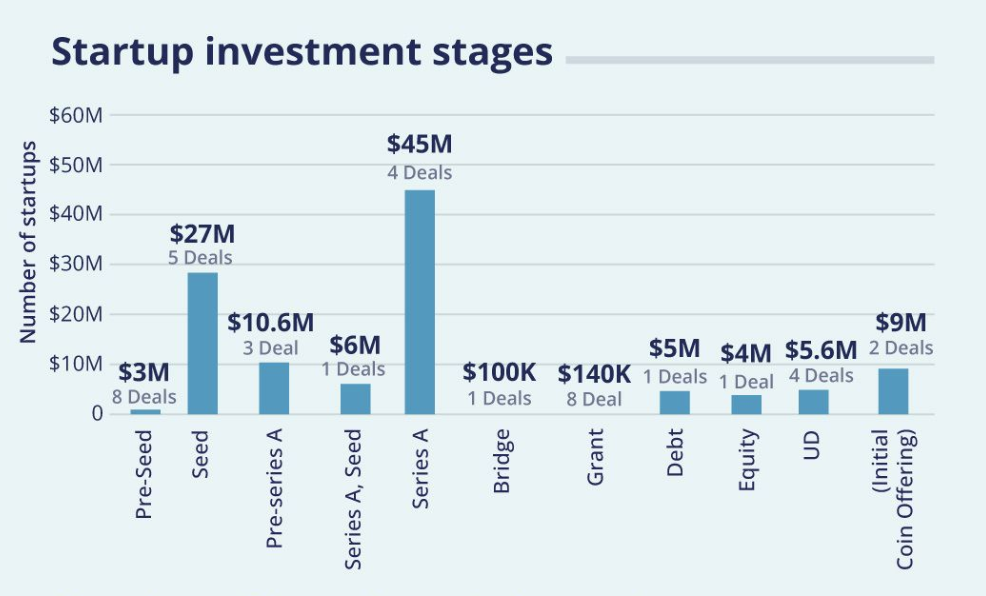

The majority of June’s investment went to the pre-Series A stage, as four startups received $45 million, followed by the Seed stage, where five startups raised $27.3 million. However, when considering investment volume, early stage startups are still capturing the attention of investors, where eight startups at their pre-seed stage garnered $3 million, and eight others received $140,000 in grants.

Startups operating the business-to-business (B2B) model dominated most of the funding in June, raising $66.4 million across 18 deals, accounting for 74 percent of the total investment, while 20 business-to-consumer (B2C) startups raised $49.5 million. As ever, male-founded startups attracted the overwhelming majority of funding, receiving $103.4 million or 89 percent of the total, while only two female-led startups raised $200,000.

What has changed in H1 2024?

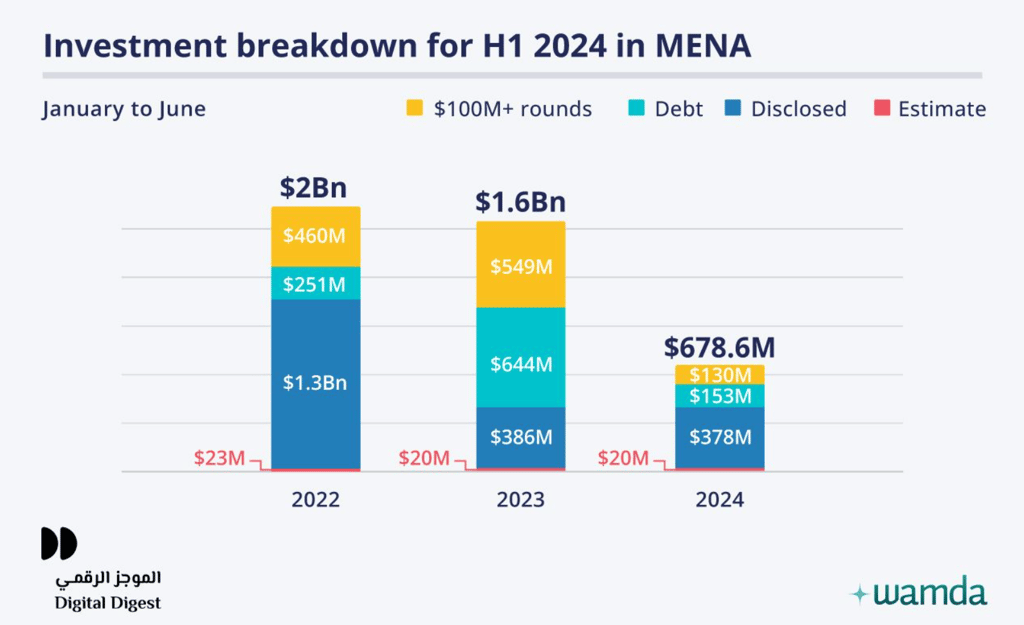

The uncertainty that has prevailed due to the war in Gaza and the potential military escalation in the region, has cast its shadow on the startup ecosystem, prompting regional and international venture capital firms (VC) to adopt a “wait-and-see” stance, which led to a 46 percent decrease in the total funding in the first half of the year, down from the $1.6 billion recorded in the same period in 2023. However, when excluding the $644 million of debt financing in H1 2023, the decline drops to 12 percent . Notably, the second quarter (Q2) of 2024 witnessed a slight surge in funding, where 98 startups raised $453 million, a 5 percent increase from Q1’s $429 million, and down by 9 percent when compared to the same period in 2023.

Where capital is concentrated

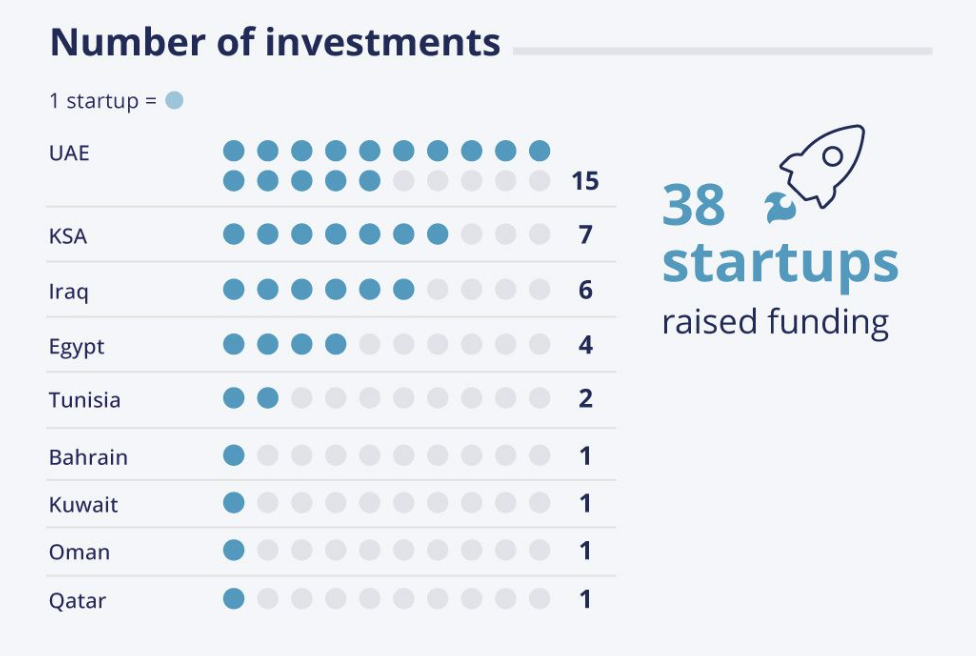

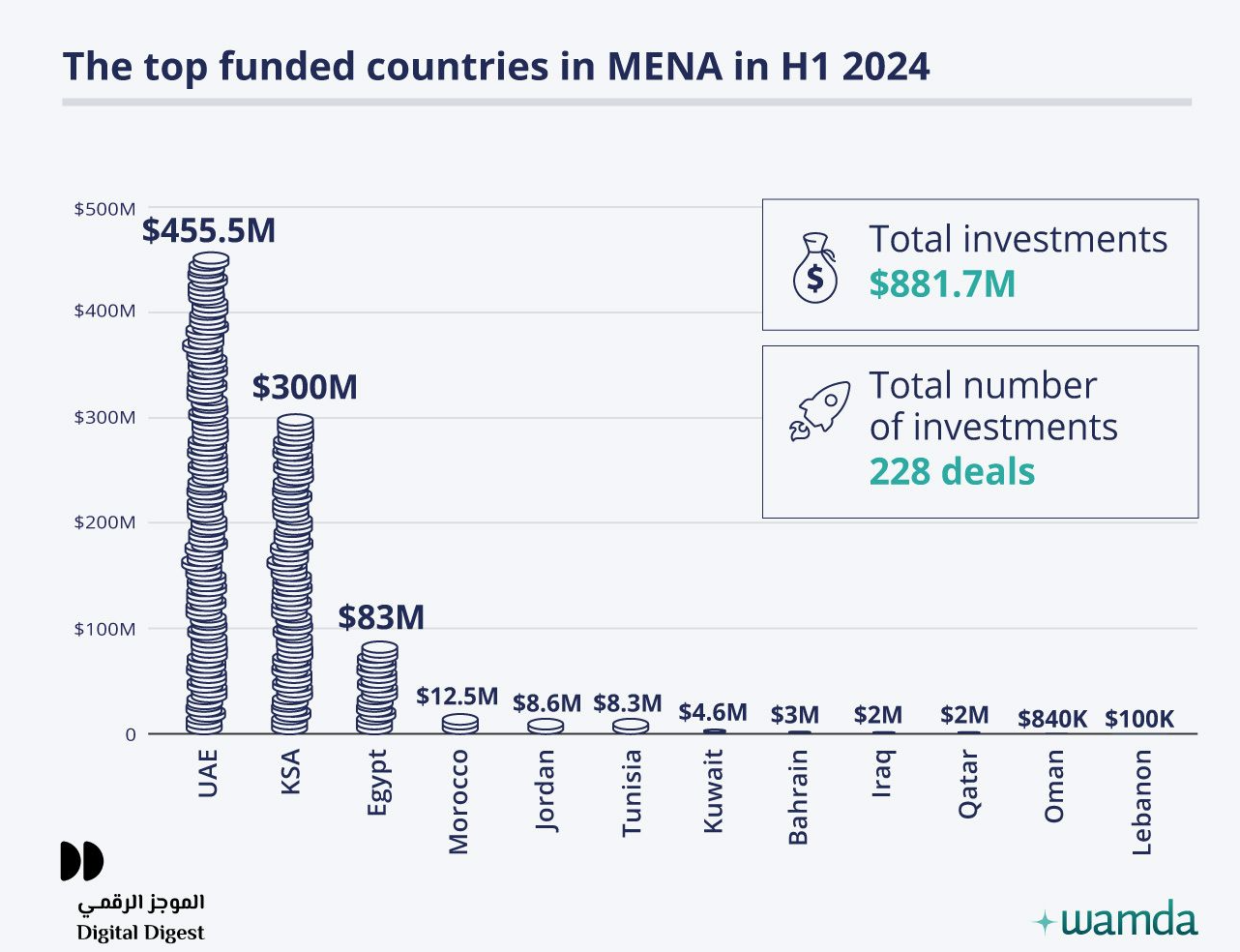

The report further found that the UAE has retained its spot as the top funded ecosystem in the region with 91 UAE-based startups raising $455.5 million in H1 2024, down from $604 million they claimed in H1 2023, followed by KSA that attracted $300 million of the total funding, down from $554 million last year. Despite the heavy investment GCC countries are pouring into the Egyptian real estate and tourism sectors, the economic crisis in the country has deepened, weighed down by a national debt absorbing 96.4 percent of its gross domestic product (GDP), and a stubborn inflation rate standing at 32.5 percent, compounded by the energy crisis that has left the country’s households in darkness for up to six hours per day.

Consequently, the Egyptian startup ecosystem drastically lost its traction in H1, with just 33 startups raising $83 million, an 80 percent decline from the same period last year. Meanwhile, the Moroccan ecosystem is gaining momentum with six of its startups receiving $12.5 million.

Sector-wise investment trends

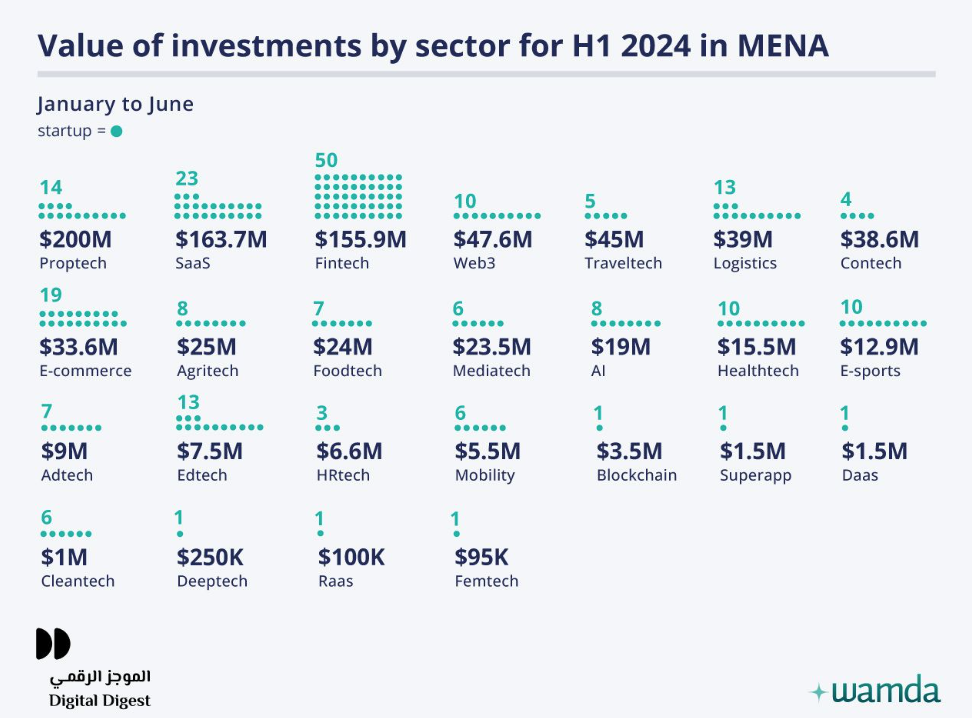

In the first half of this year, proptech emerged as a favourite of investors, attracting $200 million across 14 deals, replacing fintech as the most funded sector, which managed to raise $156 million across 50 deals. SaaS startups ranked third, attracting $164 million across 23 deals, followed by e-commerce startups which raised $33.6 million in 19 transactions, down from $194 million in H1 2023. Foodtech also witnessed a remarkable decline, dropping from $183 million in 2023 to $24 million in 2024.

Funding by stage and business model

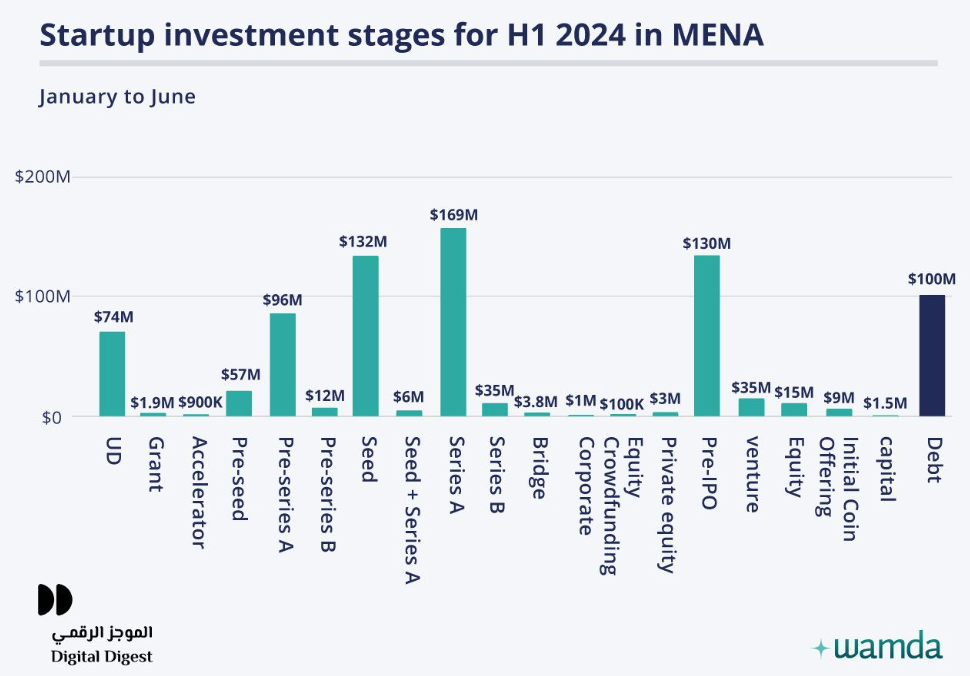

While debt financing formed 39 percent of the total funding in H1 2023, it only accounted for 17 percent of funding this year. Up to 17 Series A startups raised the majority of investment, $169 million, however, investors continue to favour the Seed stage, financing 52 Seed rounds with $131 million. The pre-Series A startups raised $96 million over 17 deals, while Salla’s pre-IPO round alone bagged $130 million.

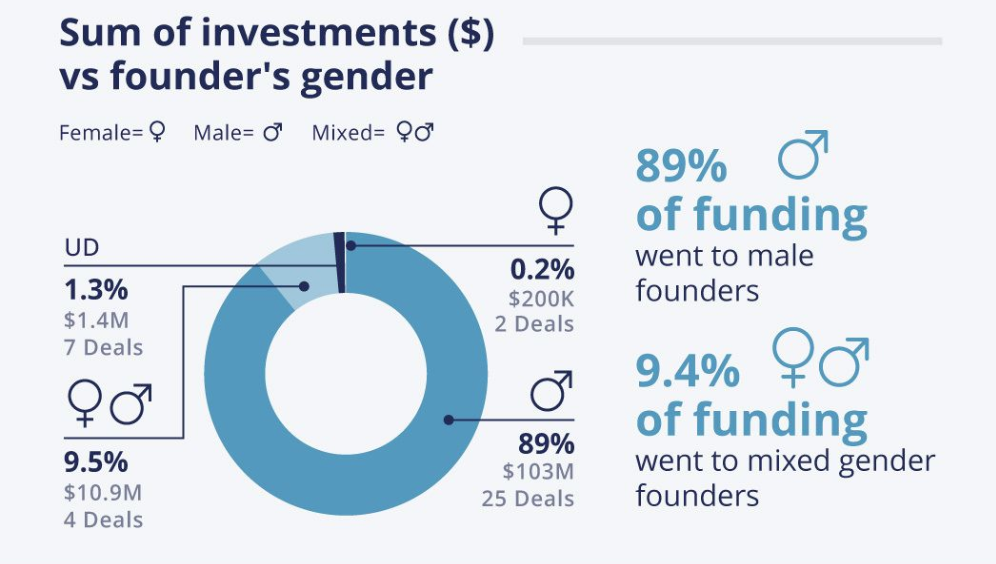

The business-to-consumer (B2C) model also was hit hard this year, raising $356 million across 86 deals, a 64 percent decline from the previous year. On the other hand, the business-to-business sector (B2B) surged by a staggering 153 percent, going from $186.6 million in H1 2023 to $473 million in 2024. Another worrying decline was the investment allocated for female-led startups, which recorded $1.8 million across 15 deals in H1 2024, down from $6 million raised by 22 startups in the previous year. Meanwhile $760 million was invested in 170 male-led startups.

Investor landscape

In the past six months, most of the capital was provided by Saudi Arabia-based VCs, contributing to 60 deals in H1, followed by UAE-based VCs, who invested in 41 deals, while Egyptian VCs participated in 24 investment deals. The U.S. was the leading foreign investor in the region, investing in 31 startups, followed by the UK, with 19 rounds recorded. Saudi Arabia-based VC RZM Investment and Bahrain’s Hope Ventures were the most active investors in H1 2024, participating in seven deals each, followed by Flat6Labs with six deals, and Disruptech with five deals.

Read more: Funding for startups at UAE’s Hub71 hit AED4.5 billion in 2022

Outlook for the remainder of 2024

The first half of the year saw a slowdown in the investment landscape, however, it is not an indication of the performance of the rest of the year. We can consider it a needed consolidation to assess the market sentiment toward each sector, or a halftime pause, so that VCs can close their funds, and investors can consider diversifying their investment portfolios based on the U.S. Federal Reserve’s interest rate. Over the past six months, several VC have launched their funds, with billions of dollars pledged to invest in tech companies in the MENA region, which will likely be reflected in Q3 investment volumes.

For more news on banking & finance, click here.