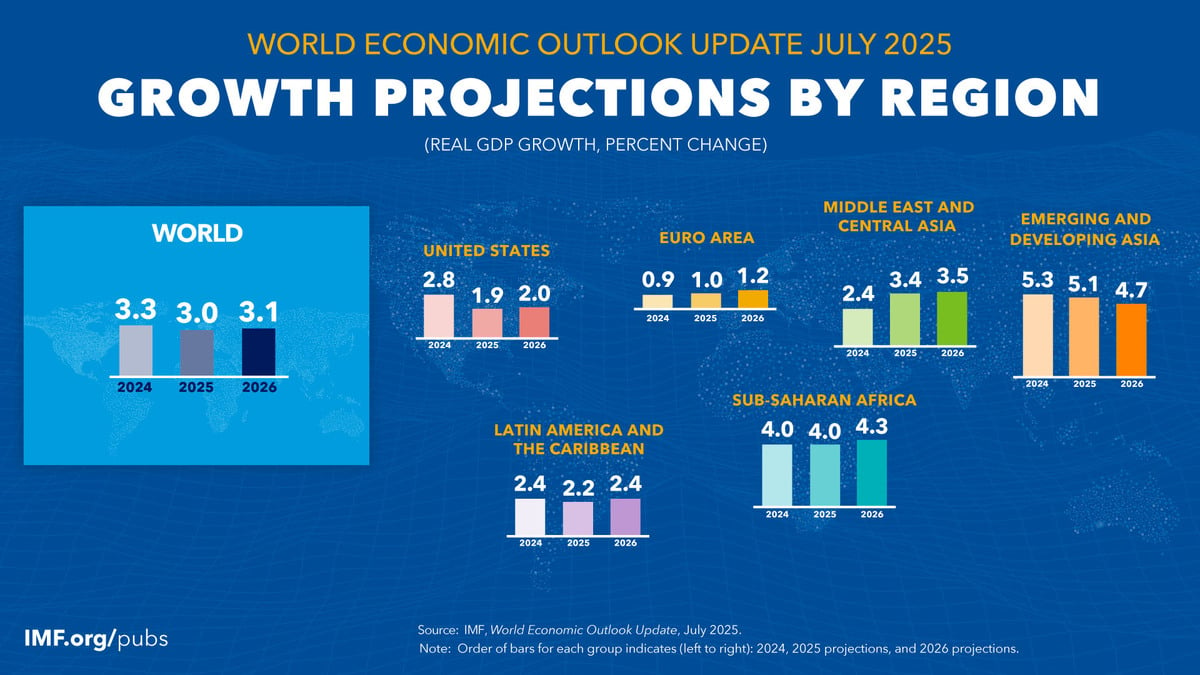

The IMF raised on Tuesday its global growth forecast to 3 percent for 2025 and 3.1 percent for 2026, up 0.2 percentage points and 0.1 percentage point, respectively, from its April 2025 World Economic Outlook.

“This reflects stronger-than-expected front-loading in anticipation of higher tariffs; lower average effective US tariff rates than announced in April; an improvement in financial conditions, including due to a weaker US dollar; and fiscal expansion in some major jurisdictions,” said the IMF.

Risks to the outlook are tilted to the downside, as they were in April, said the IMF, noting that a rebound in effective tariff rates could lead to weaker growth.

U.S. effective tariff rate dips to 17.3 percent

Since April 2025, uncertainty has remained elevated even as effective tariff rates have come down. The U.S. effective tariff rate underlying the projections is 17.3 percent, compared with 24.4 percent in the April reference forecast. Meanwhile, the corresponding effective tariff rate for the rest of the world is 3.5 percent, compared with 4.1 percent in the April reference forecast.

Despite the improvement in tariff conditions, global growth is expected to decelerate, with apparent resilience due to trade-related distortions waning. At 3 percent in 2025 and 3.1 percent in 2026, the forecasts are below the 2024 outcome of 3.3 percent and the prepandemic historical average of 3.7 percent, even though they are higher than the April reference forecast.

“The upward revision for 2025 is quite broad-based, because it owes in large part to strong front-loading in international trade as well as to a lower worldwide effective tariff rate than assumed in the April reference forecast and to an improvement in global financial conditions,” said the IMF.

MENA growth to surpass global average

Middle East and North African economies are expected to surpass the rate of global growth, rising 3.2 percent in 2025 and 3.4 percent in 2026. The report spotlights Saudi Arabia, revealing that its economy is expected to grow 3.6 percent in 2025 and 3.9 percent in 2026. Meanwhile, Egypt is set to grow 4 percent this year and 4.1 percent in the year after.

Growth in advanced economies is projected to be 1.5 percent in 2025 and 1.6 percent in 2026. In the United States, with tariff rates settling at lower levels than those announced on April 2 and looser financial conditions, the economy is projected to expand at a rate of 1.9 percent in 2025. Growth is also expected to accelerate to 1 percent in 2025 and to 1.2 percent in 2026 in the euro area.

In emerging markets and developing economies, growth is expected to be 4.1 percent in 2025 and 4.0 percent in 2026. Growth in 2025 for China is revised upward by 0.8 percentage points to 4.8 percent.

Finally, growth in the Middle East and Central Asia is projected to accelerate to 3.4 percent in 2025 and 3.5 percent in 2026, while growth is expected to be relatively stable in 2025 in sub-Saharan Africa at 4.0 percent, before picking up to 4.3 percent in 2026.

Global headline inflation to fall to 4.2 percent in 2025

The report also noted that global headline inflation is expected to fall to 4.2 percent in 2025 and 3.6 percent in 2026, a path similar to the one projected in April. The overall picture hides notable cross-country differences, with forecasts predicting inflation will remain above target in the United States and be more subdued in other large economies.

Meanwhile, world trade volume was revised upward by 0.9 percentage points for 2025 and downward by 0.6 percentage points for 2026. The near-term offset provided by front-loading of some trade flows in view of elevated trade policy uncertainty and in anticipation of tighter trade restrictions is expected to fade in the second half of 2025, with the associated payback expected to materialize through 2026.

Read: Fed expected to keep interest rates steady as tariff-driven inflation concerns persist

Risks remain

Despite revising its global growth forecast upward, the IMF noted that several risks persist. In addition to higher tariffs, elevated uncertainty could start weighing more heavily on activity, also as deadlines for additional tariffs expire without progress on substantial, permanent agreements.

Geopolitical tensions could also disrupt global supply chains and push commodity prices up. In addition, larger fiscal deficits or increased risk aversion could raise long-term interest rates and tighten global financial conditions. Combined with fragmentation concerns, this could reignite volatility in financial markets.